Assistant Fund Manager Kishan Paun examines the developing supply chain pressures emerging beneath the headlines in the Strait of Hormuz. His analysis highlights why these early disruptions may signal a far more significant and persistent global shock ahead.

When investors think about the Strait of Hormuz, they think about oil. Brent currently stands at $112 (19.03.26) and tanker traffic is down over 90%. This is widely considered to be the largest energy disruption in modern history. All true, and all completely visible, but every headline draws attention away from where the real pain is building.

Hormuz is not simply an oil corridor. It is one of the world’s most important export routes for the industrial feedstocks that sit behind food, plastics, metals, and semiconductors. These supply chains are slowly starting to creak.

Fertilisers under pressure

The Gulf exports huge volumes of urea, ammonia, and phosphate fertiliser. QatarEnergy has declared force majeure due to Iranian military attacks directly damaging key LNG production facilities, forcing the company to halt output and suspend contractual deliveries. Urea at New Orleans has jumped from $475 to $680 per metric tonne, right as the US Midwest enters its corn and soybean planting window. When fertiliser prices rise, food prices follow and consumers will face the pinch once more.

Petrochemicals, plastics and sulphur

The petrochemical exposure is just as severe. Saudi Arabia, Iran, Qatar, Kuwait, and the UAE operate 33 million tonnes of ethylene capacity, equivalent to Europe and South Korea combined. 10-12% of global polyethylene ships through Hormuz, and the region produces and exports the naphtha that Asian petrochemical plants rely on to manufacture core chemicals like ethylene. As much as 35 million tonnes of Asian ethylene capacity could lose its primary raw material input. Cars, packaging, construction, clothing are all dependent on ethylene and propylene, and both are under pressure.

Less well known is that 40% of globally traded sulphur moves through Gulf routes. Sulphur produces the sulphuric acid essential for ore leaching in the Central African Copperbelt. 90% of the sulphur imported into Zambia and the Democratic Republic of the Congo originates in the Middle East.

Semiconductors: Are energy and chemistry constraining the AI race?

The semiconductor supply chain is exposed from multiple angles. Taiwan imports a quarter of its LNG from Qatar, holds under two weeks of reserves, and generates 40% of its electricity from gas. The Taiwan Semiconductor Manufacturing Company alone consumed 8-9% of Taiwan’s total power last year. In addition, Qatar supplies 30-35% of global helium, irreplaceable in chip fabrication. The same disrupted sulphur supply feeds the sulphuric acid that semiconductor fabrication plants consume in greater volume than any other chemical. Taking it all into account, the AI race becomes meaningfully more expensive.

Why this crisis is worse than 2022

The events of 2022 when Russia invaded Ukraine, is the comparison in everyone’s minds, but this could be much more painful. In 2022, Russian oil found buyers in India and China, supply was rerouted, not removed. Now when Iran strikes a refinery, capacity is destroyed. When the Islamic Revolutionary Guard Corps (IRGC) names the Oil and Gas infrastructure of Jubail, Ras Laffan, and Al Hosn as imminent targets, as it did this week, the threat is to production itself. Most Gulf producers have no pipeline alternative to bypass the Strait.

BASF, one of the world’s largest chemical companies, based in Germany has announced price hikes of up to 30% across its European home care and industrial cleaning portfolio, citing raw material volatility, logistics costs, and soaring energy prices. Meanwhile Germany’s VCI chemical lobby warned last week of “structural collapse.” We are only three weeks into this conflict, and what we’re seeing so far are merely the early warning signs. The initial disruptions are already significant, but they likely represent just the first phase of a much broader and more persistent shock to global supply chains, energy markets and industrial production.

Positioning through the volatility

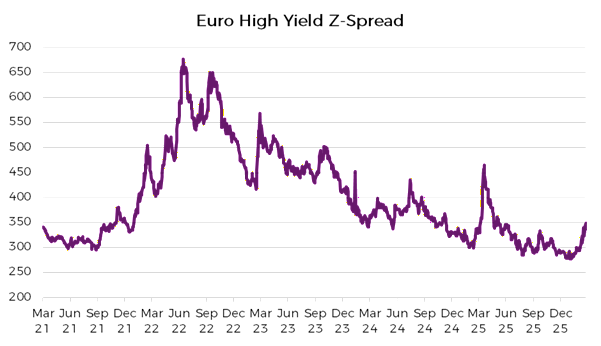

Source: Bloomberg 22/03/2021 to 18/03/2026. Past performance is not a reliable indicator of future returns.

Whilst bond yields have already repriced sharply, as the chart above shows credit spreads have not. Sterling Investment Grade credit was trading inside 65 basis points before the war and has moved only modestly. High yield has widened perhaps 30 to 40 basis points from its tights. These are not levels consistent with a sustained inflationary shock that will compress margins across chemicals, industrials, consumer goods, and any business exposed to energy and raw material costs. There is also $3trillion of corporate debt maturing this year, much of it priced on the assumption that refinancing rates would be falling and markets would be open, this environment no longer exists.

We prefer to be in high quality credit, short duration, and positioned conservatively. Investment grade over high yield with minimal exposure to the long end. Collect the carry and sit tight; we may just be getting started.