A market that looks strangely calm

It is difficult to look at the oil market today and not conclude that something is being underpriced. Brent was trading at roughly $72/bbl before the war, in a market expected to be oversupplied. Today, with the Strait of Hormuz still impaired, inventories lower, and the wider energy complex facing a separate LNG shock, Brent is only around $79/bbl. In other words, the price is not far from where it was when the market had excess supply, functioning logistics and comfortable inventories. That seems odd.

Source: Bloomberg: 27.02.26 to 18.06.26.

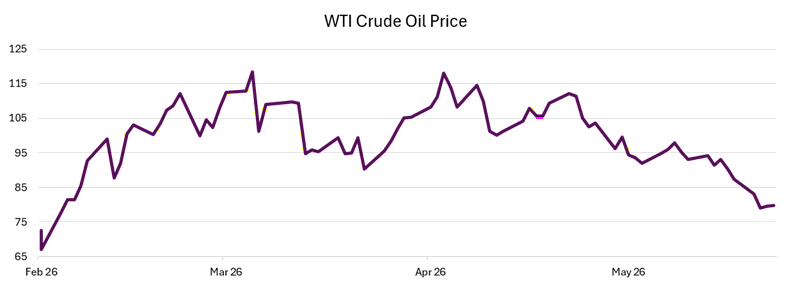

The chart above captures the point well. Brent has fallen from around $109/bbl in April to almost $80/bbl today. Some of that is perfectly rational. Markets are forward-looking, and the probability of a worst-case regional escalation has clearly fallen. It is therefore right that some geopolitical risk premium has come out of the price. The question I am less sure the market is asking is whether lower escalation risk is the same thing as a clean return to normal physical flows. I do not think it is.

Before the war, oil had a cushion. Supply exceeded demand, inventories were comfortable, and there was enough slack to absorb an initial disruption. As the conflict continued, more buffers came into play: cargoes already on the water, strategic reserve releases, weaker refinery runs in China, demand destruction in Asia, and government efforts to prevent an immediate consumer squeeze. This explains why prices did not rise even further when the shock first hit. But those buffers were not free. They were used and are now largely spent.

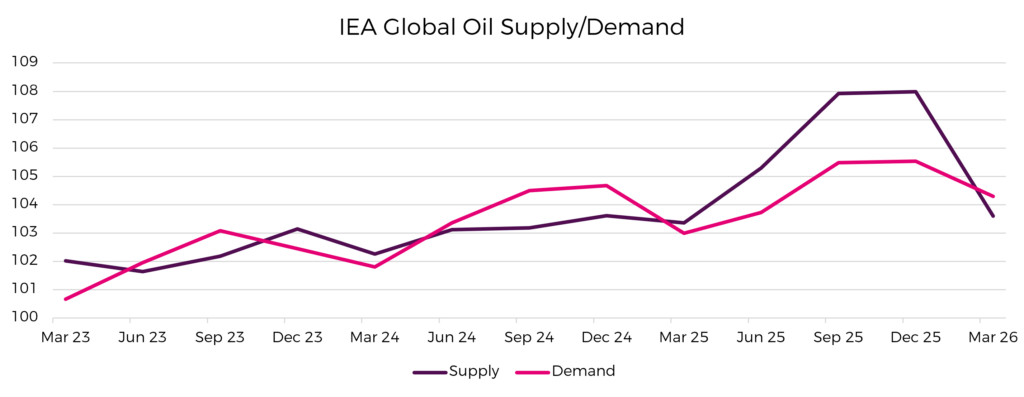

Source: Bloomberg 31.03.2023 to 31.03.26

The chart above is what makes the current price action look inconsistent. The pre-war surplus helped cushion the shock, yet the market now appears to be pricing as if that surplus still exists. Inventories have been drawn. Strategic reserves have been released. Demand has been suppressed rather than naturally balanced. This is not the same as a healthy market clearing through abundant supply.

The rebuild phase the market may be missing

What I believe market participants are overlooking is the next phase. If strategic petroleum reserves were used to dampen the spike, those barrels eventually need replacing. If commercial inventories have been drawn, they too need rebuilding. The market may be assuming that returning Middle East supply simply creates excess barrels later this year. That feels too simplistic. Some of those barrels may already have a destination: government tanks, commercial storage and refineries trying to rebuild cover.

Nor is reopening the Strait a binary event. A few tankers leaving the Gulf would be visually powerful and probably bearish for prices in the short term. But the harder question is whether ships are willing to go back in. A shipowner, insurer and crew need confidence over the full voyage, not just the day the first headline breaks. We can debate how long full trust takes to return, but it feels unlikely to be immediate.

The same applies downstream. Refineries need consistent feedstock before they raise utilisation. A global oil trader we spoke with noted that some Middle East refineries may take around three months to get back to 80% operational rates. That feels important. Whilst ships moving again would certainly weigh on oil prices, refineries are physical assets, some of which have not been used properly for three months. Restarting them is not the same as switching a screen back on.

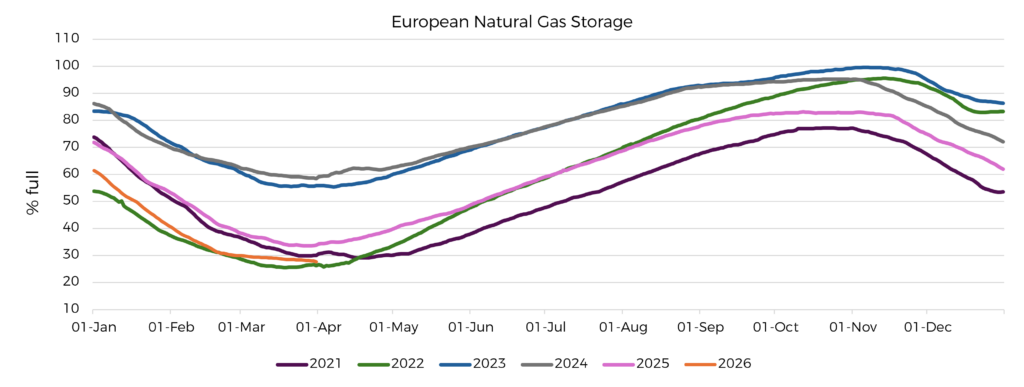

Source Bloomberg: 31.12.2021to 31.03.2026.

LNG Disruption and the Wider Energy Complex

The gas market makes the argument broader. European gas storage is near 2021 levels, well below the more comfortable post-2022 rebuild years. That alone would be uncomfortable. It is more concerning when Qatar’s LNG system has been materially impaired. Europe enters refill season from a weak starting point, while one of the world’s key LNG suppliers has 17% of its production offline for potentially multiple years. If Europe must compete more aggressively with Asia for flexible cargoes, gas prices can remain inflationary even if crude looks calmer.

This is the crux of the issue. The market is probably right to remove some geopolitical risk premium. It is less obviously right to price the physical system as though it has already repaired itself. Shipping confidence, refinery utilisation, inventory rebuilding and European gas storage do not normalise at the speed of futures markets.

We are not arguing that oil needs to revisit the panic highs.

We are arguing that $79/bbl looks too close to the old, oversupplied world. Today’s market has thinner buffers, a restocking requirement, damaged LNG supply and a product-market inflation channel that may prove sticky. The market has priced relief. It has not fully priced repair. On that basis, oil looks too low, and the energy impulse into inflation is probably not finished.